[ad_1]

We now stand on the threshold of another age of turmoil. Cash is on its way out and digital technologies replacing it can change the nature and capabilities of money. Today, central bank money simultaneously serves as a unit of account, a medium of exchange and a store of value. But digital technologies could lead to separation of these functions as certain forms of proprietary digital money, including some cryptocurrencies, gain traction. This shift could weaken the dominance of central bank money and set off another wave of currency competition that could have lasting consequences for many countries, especially those with smaller economies.

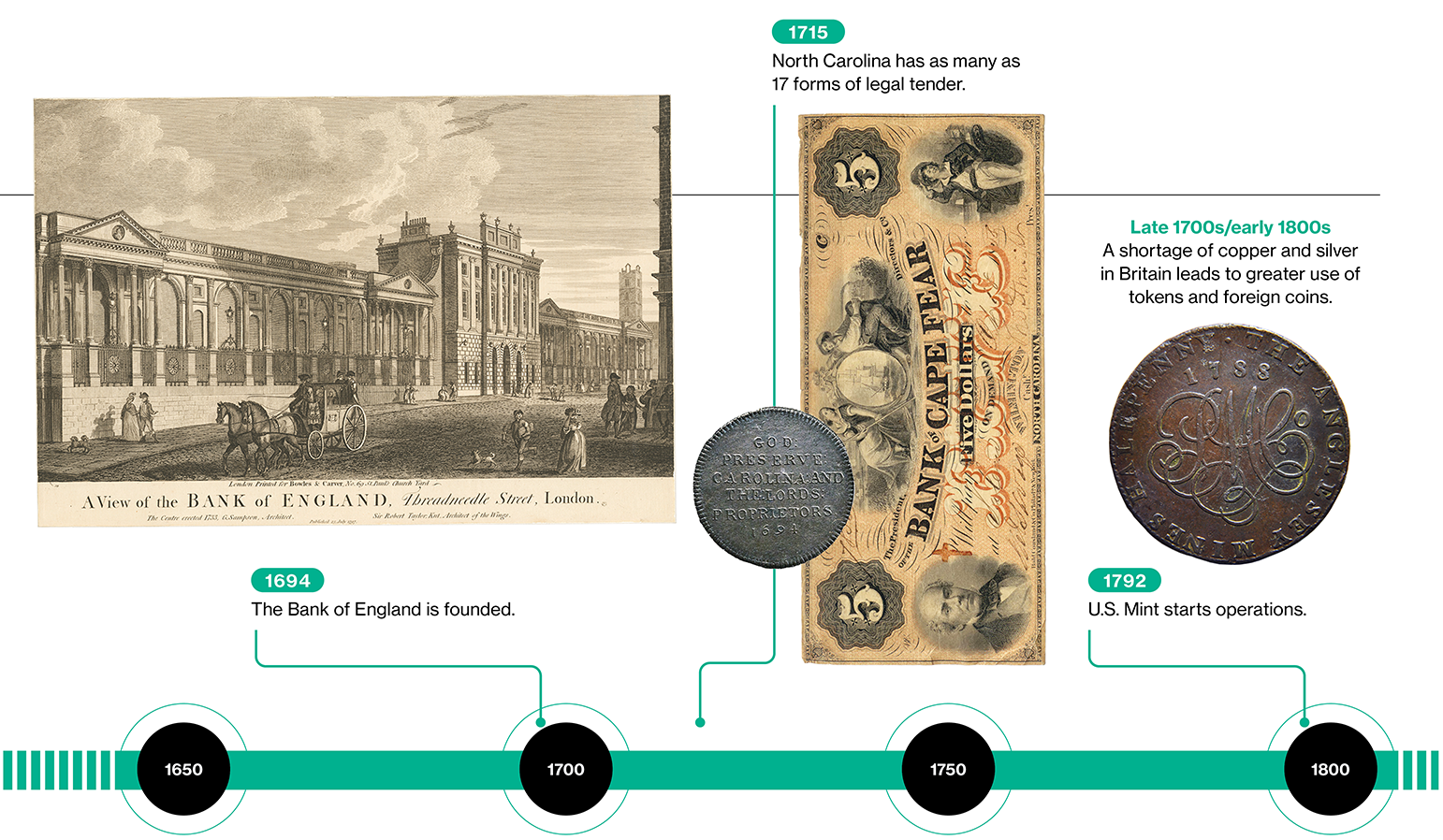

In ancient societies, objects such as shells, beads, stones served as money. The first paper currency appeared in China in the seventh century in the form of certificates of deposit issued by reputable merchants who supplemented the value of banknotes with warehouses of commodities or precious metals. In the 13th century, Kublai Khan introduced the world’s first backed paper currency. His kingdom’s bills had value because Kublai decided that everyone in his realm should accept them for payment with the pain of death.

Kublai’s successors were less disciplined than they were in controlling the release of paper money. Subsequent governments in China and elsewhere were tempted to recklessly print money to finance government spending. Such immorality typically leads to spikes in inflation or even hyperinflation, which means a sudden decrease in the amount of goods and services a given amount of money can buy. This principle holds true even in modern times. Today, it is the trust in the central bank that provides the widespread acceptance of banknotes, but this trust must be maintained through disciplined government policies.

NEW YORK PUBLIC LIBRARY DIGITAL COLLECTIONS; PUBLIC NAME; JEAN-MICHEL MOULLEC OF VERN SUR SEICHE, (35, BRETAGNE), FRANCE/WIKIMEDIA COMMONS

But to many, cash now seems largely anachronistic. Literally using physical money has become less and less common as our smartphones allow us to make payments easily. The way people in rich countries like the United States and Sweden, as well as residents of poorer countries like India and Kenya, pay even for basic purchases has changed in just a few years. This shift may seem like a potential driver of inequality: If cash disappears, it could disenfranchise the elderly, the poor, and others at a technological disadvantage. But in practice, cell phones are nearly saturated in many countries. And digital money, if implemented correctly, could be a huge financial inclusive power for households with little access to formal banking systems.

There’s still some life in Cash. Even as contactless payments become more common during the Covid pandemic, demand for cash has increased in major economies, including the US, probably as people see it as a safe form of savings. Many states in the US have laws to ensure that cash is accepted as a form of payment; this is something that will protect people who are unable or unwilling to pay by other means. But consumers, businesses and governments have generally welcomed the transition to digital forms of payment, especially as new technologies make them cheaper and more convenient.

[ad_2]

Source link